Printable Montana Pr 1 Template

Key takeaways

When filling out the Montana PR-1 form, it’s essential to be thorough and accurate to avoid complications with your tax return. Here are some key takeaways to keep in mind:

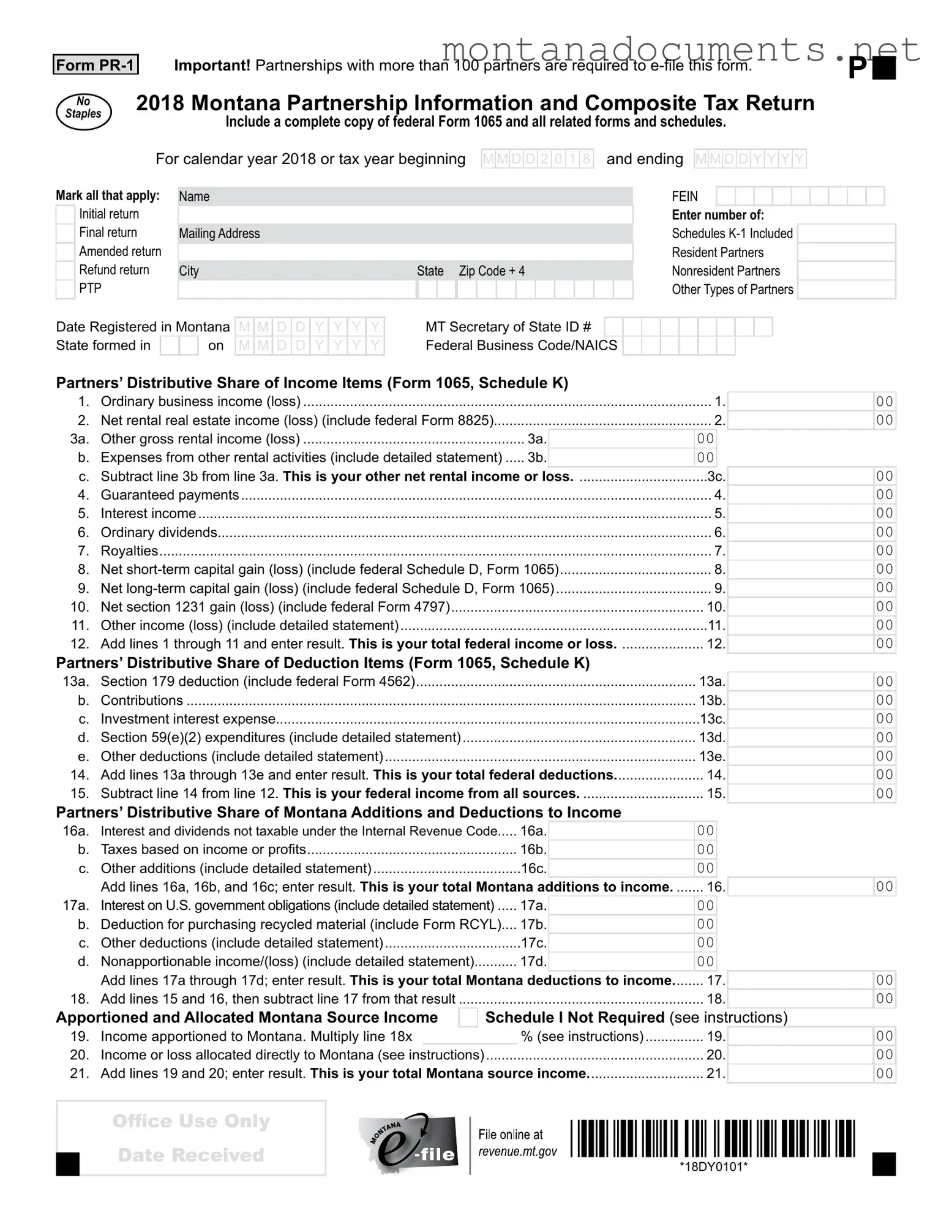

- E-filing Requirement: If your partnership has more than 100 partners, you must e-file the PR-1 form. Ensure you have the necessary systems in place to comply.

- Federal Form Inclusion: Always include a complete copy of federal Form 1065 along with all related forms and schedules. This is crucial for accurate reporting.

- Correct Marking: Clearly mark whether this is an initial, final, amended, or refund return. This helps the tax authorities process your form correctly.

- Accurate Partner Information: Provide accurate details for each partner, including their distributive share of income and deductions. This information is vital for calculating individual tax responsibilities.

- Montana Additions and Deductions: Be diligent in reporting Montana-specific additions and deductions to income. This can significantly impact your overall tax liability.

- Composite Tax Calculation: Carefully calculate the composite tax for participating partners. This involves using the correct ratios and ensuring all figures are accurate.

- Review for Completeness: Before submission, review the entire form for completeness and accuracy. Inaccuracies or omissions can lead to penalties or delays in processing.

Completing the Montana PR-1 form accurately is crucial for compliance and to minimize any potential issues with the Montana Department of Revenue. Take the time to ensure all details are correct and complete.

Similar forms

The Montana PR-1 form shares similarities with the IRS Form 1065, which is the U.S. Return of Partnership Income. Both forms require partnerships to report their income, deductions, and credits. They serve as the foundational documents for reporting a partnership's financial activities to the federal government. Just as the PR-1 requires a complete copy of Form 1065 and its related schedules, Form 1065 also demands detailed information about each partner's distributive share of income and deductions, ensuring transparency and compliance with tax obligations.

Another document akin to the Montana PR-1 is the Schedule K-1 (Form 1065). This form is used to report each partner's share of income, deductions, and credits from the partnership. Similar to the PR-1, which includes a section for listing each partner's distributive share, the K-1 provides specific details that partners need for their individual tax returns. Both documents emphasize the importance of accurately reflecting each partner's financial stake in the partnership, ensuring that all income and deductions are properly allocated.

The Montana PR-1 also resembles the IRS Form 8865, used for reporting information on U.S. persons with respect to certain foreign partnerships. Both forms require detailed financial disclosures and the reporting of income, deductions, and credits. While the PR-1 focuses on Montana tax obligations, Form 8865 addresses international tax considerations, yet they both emphasize the need for comprehensive reporting to maintain compliance with tax regulations.

Additionally, the Montana PR-1 shares characteristics with the IRS Form 1120-S, which is filed by S corporations. Both forms are designed for pass-through entities, meaning that income is reported on the owners' tax returns rather than being taxed at the entity level. This similarity highlights the common goal of ensuring that income and deductions flow through to the individual partners or shareholders, promoting a clear understanding of tax liabilities across different business structures.

The Montana Composite Income Tax Return also aligns with the PR-1, particularly in how it addresses the tax obligations of partnerships with nonresident partners. Both documents facilitate the calculation of taxes owed by partnerships and ensure that each partner's share of income is accurately reported. The composite return provides a streamlined process for partnerships to fulfill their tax responsibilities, similar to how the PR-1 consolidates essential information for Montana tax purposes.

For anyone involved in a sale, understanding the nuances of transaction documentation is crucial; thus, the Bill of Sale form plays a vital role in ensuring clarity and protection for both parties involved. This form, which can be crucial in various transactions, outlines the specifics of the sale and transfer of ownership. For more detailed information on how to effectively utilize this form, you can refer to the following resource: https://onlinelawdocs.com/bill-of-sale/.

Lastly, the Montana Schedule K-1 is another document that parallels the PR-1. This schedule is specifically designed to report each partner's share of income, deductions, and credits from the partnership, much like the K-1 associated with the federal Form 1065. Both schedules serve to inform partners about their individual tax responsibilities and ensure that the partnership's financial activities are accurately reflected in each partner's tax filings. The emphasis on clarity and detail in both documents helps to uphold the integrity of the tax reporting process.

Browse More Forms

Montana Nr 1 - The Montana NR-1 form is used for claiming exemption from income tax for North Dakota residents.

For those seeking a reliable method to document their transaction, the important Dirt Bike Bill of Sale form can be accessed through this link: a crucial California dirt bike bill of sale. This document not only secures the sale but also lays out the necessary details for both parties.

How Do I Get a Copy of My Form 1023 - Dependent children's information is collected only if the retiree does not have a spouse.

Mt Post - State the reason for leaving each job listed on the application.

Common mistakes

-

Incomplete Information: One common mistake is failing to provide all necessary information on the form. This includes not entering the complete name of the partnership, mailing address, or Federal Employer Identification Number (FEIN). Each piece of information is crucial for processing the return accurately.

-

Incorrect Partner Counts: Some individuals mistakenly report the number of partners incorrectly. It is essential to accurately count and report the number of resident and nonresident partners, as this can affect the overall tax calculation.

-

Missing Schedules: Another frequent error involves not including the required federal Form 1065 and all related schedules. This documentation is necessary to support the figures reported on the Montana PR-1 form.

-

Misclassification of Returns: Many filers fail to properly mark the type of return being submitted. It is important to indicate whether the return is an initial, final, amended, or refund return. This classification helps the tax authorities process the return correctly.

-

Calculation Errors: Lastly, calculation mistakes can occur, particularly when summing income and deductions. Double-checking the math is vital to ensure that the total federal income and deductions are accurate, as these figures directly impact the tax owed or refund due.

Documents used along the form

The Montana PR-1 form is a crucial document for partnerships operating in Montana, serving as the Partnership Information and Composite Tax Return. However, it is often accompanied by several other forms and documents that provide additional information and context for the tax filing process. Understanding these accompanying documents is essential for ensuring compliance and accuracy in tax reporting.

- Federal Form 1065: This is the U.S. Return of Partnership Income, which provides detailed information about the partnership's income, deductions, and credits. It serves as the foundation for the Montana PR-1 form, as it includes the necessary financial data required for state tax calculations.

- Schedules K-1: These schedules report each partner's share of the partnership's income, deductions, and credits. They are essential for partners to accurately report their individual tax obligations and are included with the PR-1 to show how income is distributed among partners.

- Montana Schedule IV: This schedule is used to calculate the composite income tax for eligible participating partners. It provides a breakdown of each partner's tax liability based on their share of the partnership's income, ensuring that the correct amount is reported and paid.

- Form RCYL: The Recycle Credit form is necessary for partnerships claiming tax credits related to recycling activities. It provides details on the amount of credit being claimed, which can significantly reduce the overall tax liability.

- Federal Form 4562: This form is used to report depreciation and amortization. Partnerships claiming Section 179 deductions must include this form to substantiate their claims for deductions on certain types of property.

- Montana Schedule K: This schedule is used to report the partnership's additions and deductions to income for Montana tax purposes. It helps ensure that all relevant adjustments are considered when calculating the partnership's taxable income in the state.

- Emotional Support Animal Letter: This document verifies a person's need for an emotional support animal due to a mental or emotional disability, as outlined by a licensed mental health professional. For further insights, you can refer to TopTemplates.info.

- Form 8825: This is the rental real estate income and expenses form. If the partnership has rental activities, this form is necessary to report the income and expenses associated with those activities, which is critical for accurate tax reporting.

Each of these forms and documents plays a vital role in the tax filing process for partnerships in Montana. By understanding their purpose and how they interconnect, partnerships can navigate the complexities of tax compliance more effectively, ultimately leading to a smoother filing experience and reduced risk of errors.

Misconceptions

- Misconception 1: Only partnerships with fewer than 100 partners need to e-file.

- Misconception 2: The Montana PR-1 form does not require federal forms.

- Misconception 3: All partnerships are eligible to file the PR-1 form.

- Misconception 4: The PR-1 form is only for tax returns.

- Misconception 5: Partners do not need to report their income on the PR-1 form.

This is incorrect. Partnerships with more than 100 partners are mandated to e-file the Montana PR-1 form. This requirement applies regardless of the partnership's structure or income level.

In reality, the Montana PR-1 form must include a complete copy of federal Form 1065 along with all related forms and schedules. Failing to provide these documents can lead to delays or rejections.

Not all partnerships qualify. Only those that are registered in Montana and meet specific criteria regarding income and partner residency can file this form. It’s essential to review eligibility before submission.

This form serves multiple purposes. It can be used for initial, final, amended, or refund returns. The type of return must be marked appropriately on the form to ensure proper processing.

Partners must report their distributive share of income on the PR-1 form. This includes various types of income such as ordinary business income, rental income, and guaranteed payments, among others.

Understanding Montana Pr 1

-

What is the purpose of the Montana PR-1 form?

The Montana PR-1 form is used by partnerships to report their income, deductions, and tax liability for the state of Montana. It allows partnerships to file their composite tax returns, which include information about all partners, both resident and nonresident. This form ensures that the partnership complies with Montana tax laws.

-

Who is required to file the Montana PR-1 form?

All partnerships operating in Montana must file the PR-1 form. However, partnerships with more than 100 partners are required to e-file this form. This requirement helps streamline the filing process for larger partnerships.

-

What information is needed to complete the PR-1 form?

To complete the PR-1 form, you will need several pieces of information, including:

- The partnership's name and mailing address.

- The Federal Employer Identification Number (FEIN).

- The number of resident and nonresident partners.

- Schedules K-1 for each partner.

- Details on the partnership's income and deductions as reported on federal Form 1065.

Additionally, you will need to provide information about the partnership's Montana source income and any applicable tax credits.

-

What are Schedules K-1, and why are they important?

Schedules K-1 are used to report each partner's share of the partnership's income, deductions, and credits. Each partner receives a K-1 that details their specific tax information. This information is crucial for partners to accurately report their income on their individual tax returns. It is important to include all relevant K-1s when filing the PR-1 form.

-

What should I do if I need to amend a previously filed PR-1 form?

If you need to amend a previously filed PR-1 form, you should mark the "Amended return" box on the form. Then, provide the corrected information along with any necessary explanations for the changes. It is important to file the amended return as soon as possible to avoid potential penalties and interest.

-

How can I pay any taxes owed after filing the PR-1 form?

If there is an amount due after filing the PR-1 form, you can pay online at the Montana Department of Revenue's website. Alternatively, if you prefer to pay by check, make it payable to the Montana Department of Revenue. Ensure that you include your FEIN on the check for proper processing.