Printable Montana Apls101F Template

Key takeaways

When filling out and using the Montana APLS101F form, it is important to keep several key points in mind:

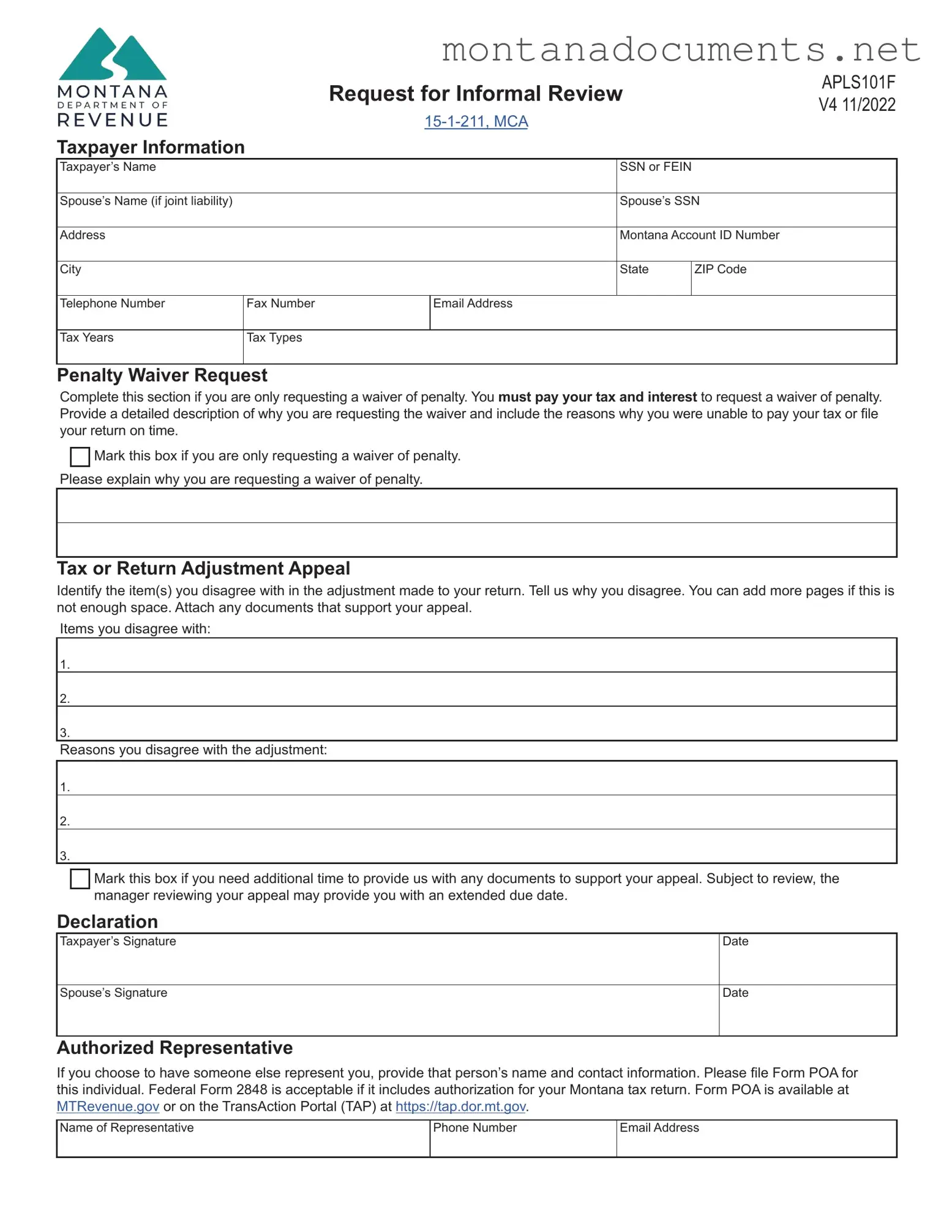

- Understand the Purpose: This form is used to request an informal review of a Notice of Assessment (NOA) or to ask for a waiver of penalty.

- Timeliness is Crucial: You must submit your request for an informal review within 30 days of receiving your NOA.

- Provide Clear Information: Clearly identify the items you disagree with and provide reasons for your disagreement. Attach any supporting documents.

- Penalty Waiver Requests: If you are requesting a waiver of penalty, you must pay your tax and interest first.

- Reasonable Cause: If you missed the 30-day deadline, you may still appeal if you can show reasonable cause for your delay.

- Signature Requirement: Ensure that both the taxpayer and spouse (if applicable) sign the form before submission.

- Authorized Representative: If you wish to have someone represent you, include their contact information and file Form POA.

- Follow Submission Guidelines: Email or mail your completed form and any supporting documents to the appropriate department address.

Being thorough and timely in your approach can significantly impact the outcome of your appeal or penalty waiver request. Take the time to gather all necessary information and ensure that your submission is complete.

Similar forms

The Montana APLS101F form, which serves as a Request for Informal Review, shares similarities with the IRS Form 843, Claim for Refund and Request for Abatement. Both forms allow taxpayers to request a review of tax assessments or penalties. While the APLS101F is specific to Montana tax matters, Form 843 is used at the federal level. Each form requires taxpayers to provide detailed explanations for their requests, along with any supporting documentation, ensuring that the reviewing authority has the necessary information to make an informed decision.

Another document akin to the APLS101F is the IRS Form 9423, Request for Appeal of Offer in Compromise. Like the APLS101F, Form 9423 is used to appeal a decision made by the tax authority. Taxpayers must articulate their reasons for disagreement and provide evidence to support their claims. Both forms aim to facilitate a fair review process, allowing taxpayers to contest decisions they believe are unjust.

The Montana APLS101F also resembles the IRS Form 12153, Request for a Collection Due Process or Equivalent Hearing. This form allows taxpayers to request a hearing regarding tax levies or liens. Similar to the APLS101F, it requires a clear statement of the taxpayer's position and supporting documents. Both forms serve as avenues for taxpayers to seek recourse against actions taken by tax authorities.

Additionally, the APLS101F is comparable to the IRS Form 8862, Information to Claim Earned Income Credit After Disallowance. This form is used when taxpayers want to claim a tax credit after it has been previously denied. Both forms necessitate a detailed explanation of the taxpayer's circumstances and a demonstration of eligibility or justification for the request. They aim to ensure that taxpayers have a chance to present their case for reconsideration.

The APLS101F is also similar to the IRS Form 8821, Tax Information Authorization. While this form primarily authorizes a representative to receive taxpayer information, it complements the APLS101F by allowing taxpayers to designate someone to assist them during the review process. This ensures that the taxpayer's interests are represented effectively, similar to the representation options available in the APLS101F.

Furthermore, the Montana APLS101F form can be compared to the IRS Form 1040X, Amended U.S. Individual Income Tax Return. Both forms allow taxpayers to correct previous tax filings and address discrepancies. They require a thorough explanation of the changes being made and the reasons behind them. The aim is to ensure that taxpayers can rectify errors and provide accurate information to tax authorities.

The APLS101F also has similarities with the Montana Department of Revenue's Form APLS102F, Notice of Referral to the Office of Dispute Resolution. This form is used when a taxpayer wishes to escalate their appeal after receiving a determination. Both forms provide a structured process for taxpayers to seek further review of decisions made by tax authorities, emphasizing the importance of transparency and fairness in the tax system.

The APLS101F form is essential for those navigating the complexities of tax appeals, similar to how a Bill of Sale form confirms ownership transfer in property transactions. Taxpayers utilizing the APLS101F must carefully articulate their circumstances and supporting evidence, ensuring clarity in their requests—much like the detailed account provided in a https://onlinelawdocs.com/bill-of-sale/ to document the terms of sale.

Another related document is the IRS Form 3949-A, Information Referral. This form allows individuals to report suspected tax fraud. While the APLS101F is used to contest tax assessments, both documents engage with the tax system's integrity. They highlight the importance of accountability and provide pathways for individuals to voice their concerns regarding tax matters.

Lastly, the APLS101F is akin to the IRS Form 2848, Power of Attorney and Declaration of Representative. This form allows taxpayers to authorize someone to act on their behalf regarding tax matters. Similar to the representation section of the APLS101F, it ensures that taxpayers can have knowledgeable representatives assist them in navigating the complexities of tax appeals and reviews.

Browse More Forms

Montana State Scholarships - Be prepared to provide your legal name and Social Security Number on the form.

The RV Bill of Sale document is crucial for anyone looking to complete a safe and legal transaction. For detailed requirements and templates, check out this resource on how to utilize an essential RV Bill of Sale effectively: essential RV Bill of Sale.

How Do I Get a Copy of My Form 1023 - Protection against errors in payments is included in the certification process.

Common mistakes

-

Omitting Personal Information: Many individuals forget to include essential taxpayer information such as their Social Security Number (SSN) or Federal Employer Identification Number (FEIN). This omission can lead to delays in processing the form.

-

Incorrect Tax Years: It is common for people to mistakenly indicate the wrong tax years they are appealing or requesting a waiver for. Double-checking the tax years is crucial to ensure that the request is relevant and accurate.

-

Insufficient Explanation for Waiver Requests: When requesting a waiver of penalty, individuals often fail to provide a detailed description of their circumstances. A vague explanation may not be convincing enough for the department to grant the waiver.

-

Missing Supporting Documents: Some people neglect to attach necessary documents that support their appeal. Without these documents, the appeal may be dismissed or rejected, as the department relies on evidence to evaluate claims.

-

Not Marking Required Boxes: Failing to mark the appropriate boxes, such as those indicating whether the appeal is for a waiver or an adjustment, can lead to confusion and misprocessing of the request.

-

Ignoring Submission Deadlines: Many individuals overlook the 30-day deadline for submitting their appeal or waiver request. Missing this deadline can result in a deemed admission of agreement with the department’s adjustment, leaving no room for further appeal.

Documents used along the form

The Montana APLS101F form is used to request an informal review of a Notice of Assessment (NOA) or to seek a waiver of penalties related to tax obligations. When dealing with tax matters, several other forms and documents may accompany this request to ensure a comprehensive approach. Below is a list of related documents that are often utilized alongside the APLS101F form.

- Form APLS102F: This form is used to request further review by the Office of Dispute Resolution after receiving a determination on an appeal. Taxpayers can file this within 30 days from the notice of determination date if they disagree with the outcome of their informal review.

- Form POA: This is the Power of Attorney form that allows a designated representative to act on behalf of the taxpayer. It is essential for those who wish to have someone else manage their tax matters during the appeal process.

- Employment Application PDF: A standardized document that allows job candidates to present their qualifications effectively. For templates and more information, visit TopTemplates.info.

- Statement of Account (SOA): This document outlines the current balance due and serves as a bill if the taxpayer does not request an informal review or pay the outstanding amount. It is crucial for understanding the financial obligations that may be under dispute.

- Federal Form 2848: This is a federal Power of Attorney form that can be used for tax matters. It must include authorization for the taxpayer's Montana tax return if it is to be accepted by the Montana Department of Revenue.

- Supporting Documentation: Any documents that substantiate the taxpayer's claims or disagreements with the adjustments made in the NOA. This may include financial statements, correspondence, or other relevant records.

- Request for Penalty Waiver: A separate written request may be submitted to seek a waiver of penalties due to reasonable cause. This document should detail the reasons for the inability to pay taxes or file returns on time.

- Informal Review Instructions: These guidelines provide detailed information on how to properly complete and submit the APLS101F form, including deadlines and the appeal process.

Utilizing these forms and documents effectively can streamline the appeal process and improve the chances of a favorable outcome. Each document plays a specific role in addressing tax disputes and ensuring that taxpayers have the opportunity to present their case clearly and comprehensively.

Misconceptions

Understanding the Montana APLS101F form can be challenging due to various misconceptions. Here’s a list of common misunderstandings and clarifications regarding this form.

- Misconception 1: The form is only for tax disputes.

- Misconception 2: You can submit the form anytime.

- Misconception 3: You don’t need to pay taxes to request a penalty waiver.

- Misconception 4: The form is only for individual taxpayers.

- Misconception 5: You can only disagree with one item on your NOA.

- Misconception 6: Submitting the form guarantees a favorable outcome.

- Misconception 7: You cannot provide additional documents after submitting the form.

- Misconception 8: You can’t appeal after missing the 30-day deadline.

This form can also be used to request a waiver of penalties, not just to dispute tax adjustments.

The request for informal review must be submitted within 30 days of receiving your Notice of Assessment (NOA).

You must pay your tax and interest to be eligible for a waiver of penalties.

Both individual and joint taxpayers can use this form, as it accommodates spouse information if applicable.

You can list multiple items you disagree with on the form and provide reasons for each.

Submitting the form does not guarantee that your appeal will be accepted; it will be reviewed and a decision made.

You can attach additional documents to support your appeal, even if you run out of space on the form.

If you miss the deadline, you can still appeal if you can demonstrate reasonable cause for your delay.

By addressing these misconceptions, taxpayers can better navigate the process and ensure they are using the Montana APLS101F form correctly.

Understanding Montana Apls101F

-

What is the purpose of the Montana APLS101F form?

The Montana APLS101F form is used to request an informal review of a Notice of Assessment (NOA) or to ask for a waiver of penalty. An NOA is sent when there is an adjustment to your tax return, a change in the amount owed, or a reduction in your refund. If you disagree with the NOA, this form allows you to initiate the review process.

-

How do I request a waiver of penalty using this form?

If you want to request a waiver of penalty, you must first pay your tax and interest. On the form, provide a detailed explanation of why you could not pay your tax or file your return on time. Make sure to mark the appropriate box indicating that you are only requesting a waiver of penalty.

-

What should I include in my appeal for an adjustment made to my return?

In your appeal, identify the specific items you disagree with in the adjustment. Clearly explain your reasons for disagreement. If necessary, you can attach additional pages or documents that support your case. It’s important to provide as much detail as possible to strengthen your appeal.

-

What happens if I miss the 30-day deadline to request an informal review?

If you do not submit your appeal within 30 days of the NOA date, it will be considered a deemed admission that you agree with the adjustment. However, if you have reasonable cause for missing the deadline, you can still request a review. You will need to provide an explanation for the delay, and the department will determine if your reasons warrant a review of the adjustment.